The market landscape

M&A: Positive signals after a slow year

M&A activity including strategic transactions and buyouts historically drives most of the aggregate deal value in the space. M&A deal flow has been relatively steady over the past decade, with a few notable spikes driven by megadeals. Activity proved more subdued in recent years, with deal value declining each year from 2020 onward, a trend exacerbated by the broader market volatility that emerged in 2022. However, signs exist that this string of declines may end.

In the first quarter of 2023 deal value represents more than half of the total closed in 2022. The initial wait-and-see approach that participants took in 2022 in response to uncertainty has waned. Dealmakers are accepting less favorable market conditions as a longer-term reality and now look to execute on deals rather than pass by smaller windows of opportunity.

While deal value grew in the first quarter of 2023, quarterly deal count dropped to its lowest point in over a decade, as dealmakers move forward only with their strongest prospects in the current market. Opportunities still exist, but for a more selective population.

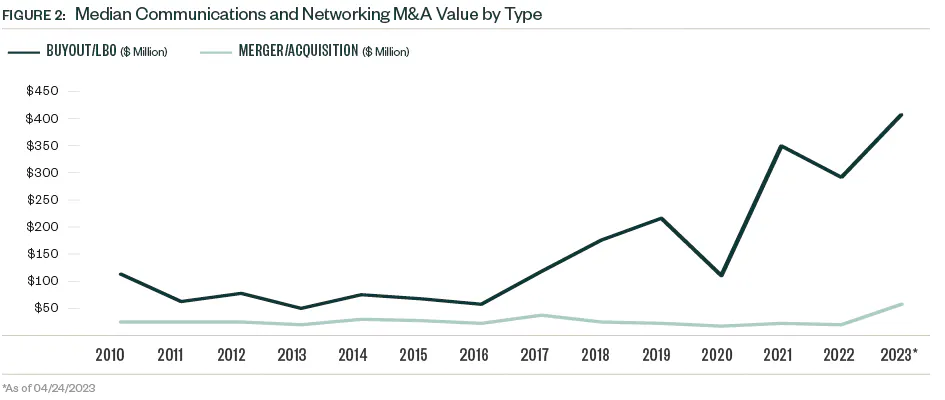

After declines in 2022, this resulted in larger median deal sizes for both buyout/leveraged buyout (LBO) and strategic categories. Deal multiples also dropped in 2022 as high valuations became more difficult to justify, and higher interest rates increased lending costs for dealmakers. The median EV/EBITDA (enterprise value to earnings before interest, taxes, depreciation, and amortization) multiple declined by more than 25% in 2022, and the median debt percentage reduced by over 800 basis points.

Strategic deals historically represent most deal count and value, though buyouts increased their share of total deal value since 2020. The buyout category also increased its share of deal count to a record 40.5% in 2022, when strategic acquisitions moved to the backburner as budget priorities shifted away from growth prospects to prepare for an economic downturn. Buyouts account for approximately one-third of total deal count and just under 50% of total deal value YTD.

PE dealmakers maintain momentum

PE activity in the industry proved far more resilient than broader market sentiment would suggest, with total deal value in 2022 coming in just shy of the record high reached in 2021. Fewer deals were completed in 2022, however, indicating that along with M&A, deals are closing for a more selective group of companies.

Following a steady level of activity in each quarter of 2022, deal value rose materially in the first quarter of 2023, reaching the highest quarterly level since Q3 2021 and the second-highest quarterly total on record, according to PitchBook data.

Buyouts and LBOs still represent most of both deal value and count, but growth- and expansion-stage deals represent a larger portion of deal count YTD. Valuations remain compressed, which leaves the window of opportunity for PE firms open, but these minority investments offer an alternative strategy for firms as macroeconomic difficulties persist.

PE firms are strongly positioned in the down market to take advantage of lower target valuations, and this has heightened competition between firms. PE deal multiples rose significantly in 2022 in this environment, including the median EV/EBITDA multiple, which grew 58.0% year over year.

Equity primarily drove this growth, with the median equity/EBITDA multiple notably almost doubling in 2022 despite broader declines in equity values. Interest rates increased the cost of debt associated with deals, and firms looked to decrease exposure. The median debt percentage of PE deals, which declined almost 10% from 2021, illustrates this shift.

The PE exit environment in the communications and networking industry can be cyclic with several peak and trough years since 2010. A precipitous drop in exit value occurred in 2022, common across industries. So far in 2023, just nine PE exits closed — a number more reminiscent of the small VC presence in the space. Market volatility continues to weigh on valuations, which creates a larger entry pipeline for PE portfolio companies but compounds difficulties down the line for those seeking exits.

Continued VC investment in innovation despite challenges

VC remains a small player in the space compared with other asset classes, but activity nonetheless hit a record $4.2 billion in 2022, compared with $4.0 billion in 2021, bucking the downward trend seen in many other industries.

Deal flow declined since then, however, and the first quarter of 2023 closed the lowest quarterly deal value since the second quarter of 2020, when the pandemic-related economic shock began.

Activity may be off to a slow start in terms of dollar value, but annual venture deal counts held steady over the past decade, and the 57 deals completed YTD indicate a flow of transactions consistent with previous years.

Powerful incumbents and exceptionally high barriers to entry exist for traditional service providers in the industry, but venture-backed companies can drive value through managed services and additive technologies including cybersecurity, Internet of Things (IoT), artificial intelligence (AI) applications, and edge computing.

The bundling of products and services and rising competitive pressures increase the innovation imperative for industry leaders, therefore driving venture investment.

Median deal sizes grew for each stage of venture in 2022 despite the challenging market conditions that emerged during the year. Companies that cleared higher hurdles for funding secured larger check sizes.

So far in 2023, sample sizes are low, and median deal sizes experienced a mixed bag of changes. The median deal size for early stage VC dropped, while that of the late-stage VC group plateaued. Late-stage deals dominate the industry’s presence in venture, representing nearly half of the total deal count and more than three-quarters of total deal value YTD.

VC exit activity in the space had a record high in 2020 and declined each year since then. Activity YTD reflects continued caution regarding exits, with just one public listing, one buyout, and four acquisitions completed.

The record levels of deal value closed in the past two years will take several years to manifest in exit activity, and compounded macroeconomic stressors continue applying pressure in the near term.