Article

New renewable energy property tax exemption in Washington state

March 10, 2024 · Authored by Marty Tschida, Shane Griffiths

Washington will implement a new exemption on the state portion of personal property tax for qualifying renewable energy facilities starting Jan. 1, 2025, per Revenue code Washington (RCW) 84.36.680. Facilities generating and storing energy must apply for and be granted the new exemption.

The exemption includes a per-month per nameplate megawatt (MW) excise tax which varies depending on the length of the exemption applied for and the energy generating method.

Who is affected by the personal property tax exemption?

This exemption applies to all solar and wind generation and storage facilities with a nameplate capacity of at least 10 megawatts.

To receive the state property tax exemption, apply with Form 64 0119 and submit it to the Department of Revenue (DOR) by March 31 of the year before the personal property tax exemption will take effect. All construction must begin on or after July 1, 2023, to be eligible.

To receive the exemption in 2025, an application must be submitted by March 31, 2024.

Background on Washington property taxation

The personal property tax exemption only applies to the state tax levy, which represents approximately 30% of a county’s annual property tax rate. Local property taxes will not be exempt and will still be billed and collected by the county treasurer.

The percentage of state tax levy that will be exempt can vary by jurisdiction. The exact percentage can be requested by calling the county that assesses the project.

The exemption does not apply to real property.

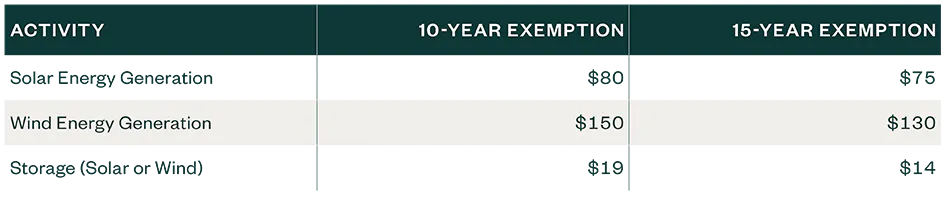

Monthly excise tax payments for exempt renewable energy facilities

During the application process, a 10-year or 15-year property tax exemption can be requested. Based on the renewable energy system and the length, the monthly excise tax payments will be as follows:

Related sections

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.