Article

An ESOP could create a quick and effective exit strategy

May 18, 2021 · Authored by Dena Herbolich, Erin Goldfarb

If you’re looking to sell your business but want to retain business continuity, you might be considering an employee stock ownership plan (ESOP) as a solution. While there are pros and cons, this is often a solution worth evaluating for businesses of all sizes.

Below, get answers to common questions about ESOPs that could help deepen your understanding of how they can be used as a quick and effective exit strategy for your business.

What are ESOPs?

ESOPs allow private company owners to sell all, or a portion, of their company to their employees. This strategy quickly and effectively creates a market for the company’s stock without having to wait months or years to find a buyer.

In addition, the sale can still be structured in a way that retains employees, keeps business owners involved if they so desire, and reduces the tax burden of the transaction — all while maintaining a fair price.

How does an ESOP function as an exit strategy?

Imagine this not-so-uncommon scenario: You own part or all of a company and want to cash out by selling your ownership interest. Maybe you’re nearing retirement and the investment in your company is your biggest asset.

If it’s a private company, typically one of the biggest challenges is finding a buyer because there’s generally no market for the stock. If you also want to maintain your legacy and management team, a sale to private equity or a strategic buyer may not be an option. Your management team may also not have the funds to buy the company.

In an ESOP purchase, ownership is transferred through the creation of an employee stock ownership trust (ESOT) that may ultimately purchase the company at fair market value. A financial advisor helps owners determine the appropriate value.

Consistent with the principle of an arm’s length transaction, in which buyers and sellers act independently without one party influencing the other, guidelines established during the formation of the trust forbid it from paying more than the advisor’s stated value for the company.

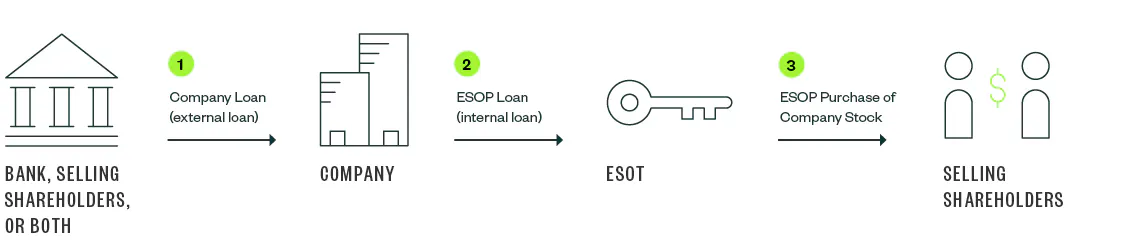

In a typical leveraged ESOP transaction, the company borrows money from the bank, selling shareholders or a combination of the two. The company then loans that money to the ESOT, and the ESOT then gives the money to the seller in exchange for the stock.

Related sections

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.