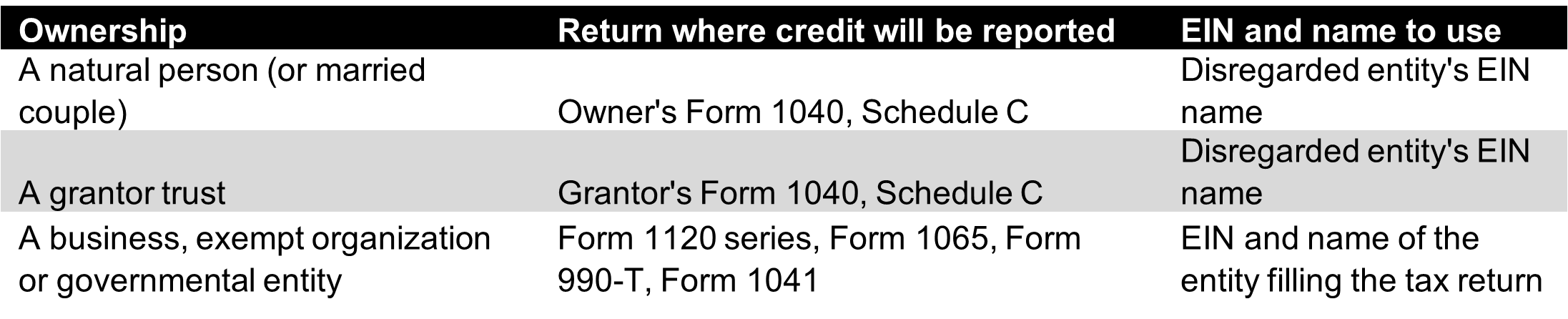

Credit-specific information

After the general registrant information is complete, based on the responses the credit-specific information portion of the application will be generated.

Note: The section 45Y, Clean Energy Production Credit, section 45Z, Clean Fuel Production Credit and section 48E, Clean Energy Investment Credit will not be included for pre-filing registration until after Dec. 31, 2024.

In order to capture the information needed for the registration, the portal offers two ways to upload the information, manual entry and bulk upload. Currently, only credits under sections 30C, 45, 45W, and 48 are available for bulk upload.

When using manual entry, all information regarding a facility or property must be manually entered into the portal. If using the bulk upload, a spreadsheet may be used to upload the information in a single step.

For the majority of credits, the following information will be needed:

- Choice of election (either elective pay or transfer)

- Subsidiary in a consolidated group of corporations

- Date construction began

- Date placed in service

- Facility/property location

- Joint ownership

- Source of funds

Aside from the information listed above, each credit type will request supporting documentation to be uploaded. An overview of each credit and supporting documentation can be found below.

Note: If detailed project plans or contractual agreements are the best support that the taxpayer is engaging in activities or making tax credit investments that qualify the registrant to claim a credit, the registrant should submit an extract of the document showing the name of the taxpayer, date of purchase and identifying information such as serial numbers, rather than the entire document.

Section 30C, Alternative Fuel Refueling Property

- 11-digit population census tract identification number

- Fuel type

In addition, the following is a non-exhaustive list of documents that may support the registration of a facility/property for the section 30C credit:

- A construction permit that clearly ties the facility/property to its physical location

- Equipment purchase documentation that shows the taxpayer as the buyer identifies the seller and specifically identifies the purchased property

- A permit issued by a government authority with jurisdiction over the operation of alternative fuel refueling properties in the community where the facility/property is located

Section 45, Renewable Electricity Production Credit

- Attestation is required the taxpayer has not claimed a section 48 credit for the facility for any prior tax period

- Type of facility (such as geothermal, solar, trash, etc.)

Supporting documents:

- Permits to operate from a utility (only if connected to the grid)

- If not connected to the grid electrical permits to operate from an authority having jurisdiction

- A brief description of the facility/property signed by an executive-level representative of the taxpayer

- Executive summary of an independent engineer or commissioning report

- An executive summary, of the interconnection agreement with the applicable utility, signed by an executive-level representative of the taxpayer

- A document, signed by an authorized representative of the supplier of materials used for the manufacture of components with regard to domestic content of such materials

Section 45Q, Carbon Oxide Sequestration

- The type of sequestration activity must be selected.

- Information regarding the ownership of the sequestration point must also be input. If the taxpayer is not the owner of the sequestration point, the operator's name and address must be input

Supporting documents:

- Approved life cycle analysis (LCA), or summary, if the LCA is greater than five pages

- Substantiation that the taxpayer will have use of the land where the sequestration facility is located, such as proof of land ownership or long term lease

- Substantiation of EPA permit application

- Proof of approval for geologic sequestration wells

- State and local government approvals or permits, including environmental approvals

Section 45U, Zero Emission Nuclear Power Production Credit

The credit under 45U applies to electricity produced and sold after Dec. 31, 2023. Due to the applicable tax years for the credit, the registration tool should not be used for a facility with an annual accounting period beginning in 2023 even if the electricity was produced in 2023.

Supporting documents:

- Copy of the license or permit issued to the taxpayer by an appropriate government agency authorizing the registrant’s operation of the Zero Emission Nuclear Power facility

Section 45V, Production of Clean Hydrogen Credit

The type of facility/ property will need to be input as a brief description of the production facility.

Supporting documents:

- Operating permit

- Commissioning report

Section 45W, Commercial Clean Vehicles Credit

Each vehicle requires its own registration number and VIN assigned by the qualified manufacturer. There is a bulk upload option available.

Supporting documents:

- Certificate of title showing ownership of the vehicle/machinery (including a certificate of title indicating a lien held by a financial institution or other lender)

- Time of sale documents, including a bill of sale or similar purchase agreement

- If registered for on-road use, a copy of a registration document issued by an appropriate government authority

Section 45X, Advanced Manufacturing Production Credit

The pre-filing registration for a section 45X credit requires an attestation that a section 48C, Qualifying Advanced Energy Project Credit will not be claimed for this property/facility for the current or any prior taxable period.

You may select as many eligible components listed under the Facility/Property Information as applicable. Election under section 45X(a)(3)(B) must be selected as “yes” or “no” during the registration process.

Supporting documents:

- Proof of ownership of the premises

- Permits to operate the manufacturing facility or to produce certain eligible components

If the production tax credit relates to an offshore wind vessel, additional supporting documents are required.

Section 48, Energy Credit

Supporting documents:

- Proof of ownership of the facility/property with respect to which the credit is computed

- Construction permit showing commencement of construction

- Permits to operate from the utility (only if connected to the grid, or if not connected to the grid electrical permits to operate from an authority having jurisdiction)

Section 48C, Qualifying Advanced Energy Project Credit

The control number issued by the Department of Energy is required to support the pre-filing registration for a credit under section 48C.

Section 48D, Advanced Manufacturing Investment Credit (CHIPS Act)

An attestation is required that the taxpayer is an “eligible taxpayer.” The attestation must include (1) the taxpayer is not a foreign entity of concern (as defined in section 9901(6) of the William M. (Mac) Thornberry National Defense Authorization Act for Fiscal Year 2021, as amended by section 103 of the CHIPS Act), and (2) has not made an applicable transaction (as defined in section 50(a)) during the taxable year.

Placed in service date must be input.

Supporting documents:

- Permits to operate from authority having jurisdiction

- EPA permit to operate (for a semiconductor manufacturer only)

- Evidence of ownership that contractually ties the qualifying property to the land and that geographic location. List relevant contracts and clauses