Excise tax

Most private foundations are subject to a 1.39% excise tax on their net investment income. Activity — both income and expenses or deductions — from alternative investments would be included in a private foundation’s calculation of net investment income.

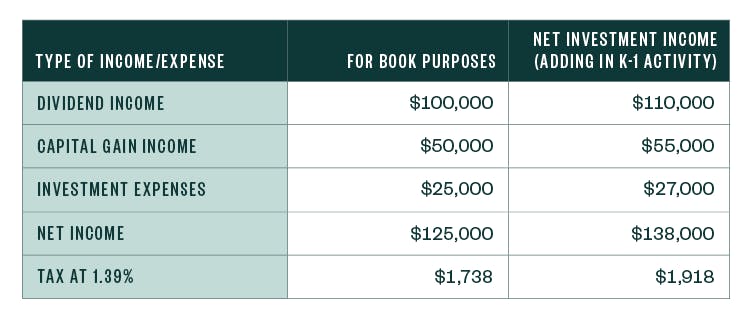

If the activity from an alternative investment isn’t booked to a private foundation’s financial statements, that activity will need to be added when the private foundation calculates its net investment income.

For example, a private foundation included in its financial statements the following activity from its traditional investments:

- Dividend income of $100,000

- Capital gain income from the sale of investments of $50,000

- Investment-related expense of $25,000

In addition, the private foundation has an alternative investment whose K-1 shows $10,000 in dividend income, $5,000 in long-term capital gains, and investment expenses of $2,000. That activity would be added to the book income to calculate the total net investment income.

From this example, the K-1 activity added a net of $13,000 to the net investment income calculation, increasing the excise tax calculation by $18.

Unrelated business taxable income

Alternative investments can generate unrelated business taxable income (UBTI) in two ways. The first is through debt-financing, either by the investment, or by the private foundation.

Generally, passive income from an interest in a partnership, such as interest, dividends, royalties, rents, and gains from the sale of securities are excluded as UBTI. But when an investment fund incurs debt to purchase investment assets, the income generated by those debt-financed assets, including passive income, are UBTI.

In addition, the private foundation may take out a loan to purchase the alternative investment, and then all the income from the investment is UBTI, regardless of the type of income.

The second way that alternative investments generate UBTI occurs when the investment operates a for-profit business. This income is generally UBTI even if the private foundation doesn’t directly participate in the for-profit business. While both are common within alternative investments, debt financing that causes UBTI happens more often.

Analyzing Schedule K-1

It’s important for private foundations to review the Schedule K-1 to determine whether the alternative investment generates UBTI, particularly the following areas:

- Line J, Partner’s share of profit, loss, and capital. Information here may determine whether the alternative investment’s activity can be aggregated for UBTI purposes, or whether the private foundation has an excess business holding.

- Line K, Partner’s share of liabilities. Information here may determine whether the alternative investment has debt financing.

- Box one – Ordinary business income (loss). Amounts in this box represent the private foundation’s share of income from some type of for-profit business operated by the alternative investment.

- Box 11 – Other income (loss). Amounts reported here may also be UBTI.

- Box 13 – Other deductions. Amounts reported here may be used as deductions against income reported in Boxes one and 11.

- Box 20V – Unrelated Business Taxable Income. This box represents the amount of taxable UBTI for the private foundation.

- Footnotes to the K-1. Information for Box 20V may be broken down in more detail in a footnote. In addition, K-1’s may have footnotes related to state-specific UBTI and foreign activity and foreign filings.

For most alternative investments, unrelated business taxable income will be reported in Box 20, Code V on the Schedule K-1, with additional information provided in a Box 20, Code V footnote.

As an example, the Box 20, Code V line may show UBTI of $20,000. It could also be broken down in a footnote as follows:

STATEMENT REGARDING UNRELATED BUSINESS TAXABLE INCOME FOR TAX-EXEMPT PARTNERS

Box 1: Ordinary Business Income $15,000 Box 6A: Ordinary Dividends $10,000 Box 13: Other Deductions $5,000

In total, this footnote also shows UBTI of $20,000. UBTI is reported on Form 990-T, and filed separately from the private foundation’s Form 990-PF. For tax-exempt corporations, UBTI on Form 990-T is taxed at the corporate tax rate, which is 21% in late 2021. At this rate, the UBTI of $20,000 in the example would generate tax of $4,200. For foundations set up as trusts, UBTI would be taxed at trust tax rates, which are graduated and top out at 37%, as of late 2021.

Occasionally, partnerships may not show an amount in Box 20, Code V, but still show an amount in Box 1, Ordinary Business Income, which represents the share of income generated from a for-profit business.

In these instances, the amount in Box one as well as any deductions in Box 13 related to the for-profit activity generally would make up the UBTI on the Schedule K-1 as the for-profit business likely is not related to the charitable mission of the foundation.

If the alternative investment is organized for tax purposes as an S corporation, the private foundation will also receive a Schedule K-1 similar to partnerships.

Unlike with partnerships, where passive income wouldn’t be UBTI unless there’s debt financing, all activity reported on the Schedule K-1 for an S corporation is UBTI to the private foundation. For this reason, it’s rarely recommended that private foundations invest in S corporations.

UBTI silos

As part of the tax-reform act enacted in December 2017, exempt organizations that have more than one unrelated business activity are required to compute their UBTI separately by activity, also known as siloing. Previously, exempt organizations could aggregate unrelated trades or business, allowing losses from one activity to offset income from another activity.

Under the final regulations for this new law, investment activities can be aggregated as one UBTI activity if they’re:

- Qualifying partnership interests (QPI)

- Qualifying S corporation interests

- Debt-financed properties

A QPI occurs when an exempt organization holds a direct interest in a partnership that meets either the de minimis test or the participation test. Under the de minimis test, an organization can hold no more than 2% of the profit interest or 2% of the capital interest in a partnership.

Under the participation test, a partnership is a QPI if the organization holds no more than 20% of the capital interest and doesn’t significantly participate in the partnership.

For additional information on aggregating investment activities for UBTI reporting purposes including how to determine significant participation, please see our article, IRS regulations on unrelated business taxable income siloing.

An organization determines its percentage interest for both tests by taking the average of the beginning of the year interest and the end of the year interest, as shown in Line J on Schedule K-1.

An S corporation holding may be aggregated with other investment activities if the ownership interest meets the same de minimis test or participation test as a QPI.

State reporting requirements

When an alternative investment has UBTI, information on state UBTI is often included in the footnotes of Schedule K-1. A private foundation may not have a presence in a state, but a holding in an alternative investment may create a corporate or trust income tax filing obligation in states with UBTI.

In addition, sometimes the alternative investment will pay withholding tax to a state, and this information is also listed in the K-1 footnotes.

Some states don’t have an equivalent of the Form 990-T. In these cases, the private foundation would file a state corporate or trust tax return.

Foreign reporting requirements

An alternative investment may itself be a foreign entity, or it may invest in other foreign entities. In either case, foreign reporting requirements may be triggered depending on the ownership percentage in the investment or on direct and indirect transfers of cash or other property to a foreign entity. Penalties for failing to file foreign forms are significant.

The following are among the more common foreign forms.

Form 926, return by a U.S. transferor of property to a foreign corporation

This form is required to report transfers of cash or property to a foreign corporation — either when the organization owns at least 10% of the foreign corporation or when the amount transferred is more than $100,000 during the 12-month period ending on the date of the transfer.

In addition to a foundation making a direct investment in a foreign corporation, a foundation may also have to file the form if a partnership it owns makes such a transfer. The penalty for failing to file a Form 926 is 10% of the amount transferred, capped at $100,000, unless the failure to comply is because of intentional disregard.

Form 5471, information return of U.S. persons with respect to certain foreign corporations.

This form is required when the U.S. investor owns 10% or more of a foreign corporation. Penalties for failure to file range from $10,000 to $50,000.

Form 8865, Return of U.S. Person with Respect to Certain Foreign Partnerships

This form is required when a U.S. investor contributes more than $100,000 to a foreign partnership in the 12-month period ending on the date of the transfer.

The form is also required if the U.S. investor owns 10% or more of the partnership.

If an alternative investment makes a transfer to another foreign partnership and files Form 8865, then its partners won’t have to report the transfer. Penalties range from $10,000 to $100,000 for failure to file, with additional penalties if the failure to file is because of intentional disregard.

FinCEN form 114, report of foreign bank and financial accounts (FBAR)

This form is for U.S. taxpayers who have offshore accounts — foreign bank accounts, brokerage accounts, and mutual funds.

Individuals who have signature authority over the accounts also have a filing obligation. The penalty for failure to file can be as high as 50% of the value of the account.

What are audit implications of alternative investments?

When private foundations invest in alternative investments, their managers also need to ensure that their financial statements properly reflect those holdings. The existence and the valuation of an alternative investment is the responsibility of the private foundation’s management.

With respect to existence, the auditors will be required to determine that the investments exist at the financial statement date and that the related transactions have occurred during the period. With respect to valuation, the auditor will need to determine if the investments are accurately stated at fair value. This is often more complicated as alternative investments are not publicly traded on an active market.

Because management is responsible for these aspects, management must have proper controls in place and an adequate understanding of the investments the foundation is making. A foundation can develop this understanding by performing due diligence on the investment before purchasing it; monitoring the investment continuously; and having financial reporting controls related to the accounting and reporting of the investment.

For the auditors, they will need to evaluate the adequacy of the foundation process to support the valuation and existence of the alternative investments. The auditors will also have to evaluate the quantity and quality of the audit evidence available. The auditors’ risk assessment should consider factors such as:

- Materiality of the alternative investments

- Nature and extent of management’s process and controls related to alternative investments

- Degree of transparency available to management to support its valuation process

- Complexity and liquidity of the alternative investments