Article

Public-entity reporting requirements could create complexity for not-for-profits

June 25, 2019 · Authored by Melissa Harman

In 2019 and 2020, adoption dates are approaching for accounting-standards changes the Financial Accounting Standards Board (FASB) introduced in 2013. While that may seem like old news, there are some public-entity classification requirements that could create complexities for not-for-profit (NFP) organizations.

While the FASB’s reporting requirements only apply to public entities, many not-for-profit organizations qualify as public entities without knowing it — meaning they’re responsible for adopting the standards.

Here are key public-entity classifications, information about the standards, and reporting details your organization should know.

Background

In 2013, the FASB issued an accounting standard update that amended its Accounting Standards Codification (ASC) Master Glossary to include the definition of a public business entity. In doing this, the FASB purposefully excluded NFP organizations from its definition to allow for flexibility in the application of standards in future years.

Because of this exclusion, many NFP organizations, including institutions of higher education, weren’t affected by the accounting standards and effective adoption dates applicable to public businesses. However, accounting standards and effective dates for public entities still apply to an NFP if it qualifies as a public entity.

Public-entity classifications

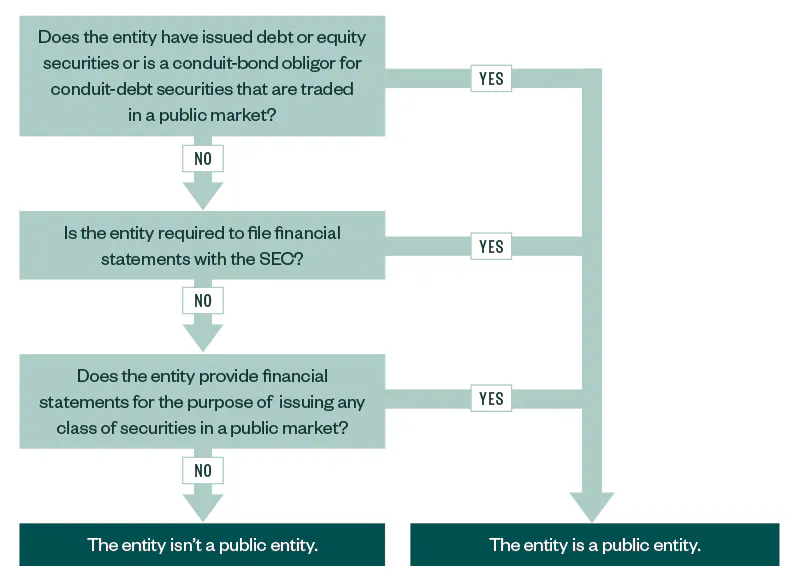

The ASC includes a couple definitions of a public entity. However, for this article, we’ll defer to only one definition, which classifies a business entity or NFP as a public entity if it meets a series of conditions, as shown in the below flow chart.

Additional definition

The ASC’s alternate definition for a public entity is used for certain ASC Topics. It’s slightly different from the above definition, noting an entity is a public entity if it meets any of the following criteria:

- Has equity securities that trade in a public market, either on a domestic or foreign stock exchange or in an over-the-counter market, including locally or regionally quoted securities

- Makes a filing with a regulatory agency in preparation for the sale of any class of equity securities in a public market

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.